Interview with Fit Pro Financial

Matt: Chad and James, really appreciate the two of you sharing your time. For those who haven’t come across the two of you before let's kick this off with going over your backgrounds.

Chad Landers: I’ve been a personal trainer in Los Angeles for 27 years and have owned a personal training studio, Push Private Fitness, for almost 17 years now. In 2018 I was named NSCA Personal Trainer of the year. I’ve been reflecting on this a lot lately because I’m sort of a unicorn in the industry by having such a long career. For context, the average career for personal trainers is less than three years. So, I started to think about what I could do to help other personal trainers have careers as long as mine and I realized that there’s a big gap in financial education and financial management in our industry. Finance has always been an important part of what I do as a business owner. I have a 401 K and a profit sharing plan setup for my business. My wife is a union employee with a union pension and a 401 K. We’ve seen the value in saving and investing and how much it’s paid off for us over our careers. That’s a perspective that’s really tough for a younger personal trainer to have. You’re so focused on the next rent check or the car payment. It’s easy to forget how valuable it is to save. With Covid-19 currently shutting down our industry we’re all seeing just how valuable it was to have saved up for years before this by keeping an emergency savings fund, just in case. So, after 27 years working in the industry I’m going to be spending time helping as many personal trainers as I can to survive this and best position themselves for the future from a financial standpoint.

James Krieger: I’ve been in the industry for a long time as well. I first started to get my feet wet in the early 90’s. I was involved in some of the really early internet forums focused on fitness and nutrition (laughing). In college my initial goal was to pursue a career in computer science, which I eventually lost interest in, and then switched my major to exercise science. I didn’t really know what I wanted to do for a career with this, but I had a real knack for science and research. I earned a grad degree, then a masters, ended up getting a research position at a highly successful weight management program and my career took off from there. Back around 2007-2008 I had a little extra cash. I remember I had just thrown some in a Fidelity account, picked a few stocks, and it was performing just ok. In parallel I was a member of this website called Covester which allowed you to link your stock account and measure your performance against other investors. There was this one guy who was just blowing away everyone at the time, Tim Sykes. I was interested in what he was doing to get these amazing returns so I started following him a lot closer. At the time he was mostly trading really low stocks, penny stocks up to stocks at less than $5 a share. Micro-caps and small-caps. So, I started to learn how to trade these stocks part-time in parallel with my job. I live on the West Coast and the market opens at 6am so I had a few hours to trade stocks before I had to go to work at 9am. I continued to do this for a while and eventually was doing well enough where I realized I could try to do this for a living. I made the jump in 2013 when I was doing really well and quit my day job to become a day trader. I was doing really well for a while and was even ranked as a top 20 trader on a website called Profitly. Unfortunately I started to become overconfident and was trying to compete with other traders instead of just focusing on what I was doing well. I started to take larger and larger positions, had a massive blowup in 2014, and closed out my day trading career. I went back full bore into the fitness industry and built my Weightology business. I always had in the back of my head an interest to trade again because I knew I could be a good trader. I just had to get out of my own way. Eventually I started practicing trading again by paper trading for a full year, just working on my strategies without trading with real money. I wanted to prove to myself that I could make money consistently for a long period. So, once I had built Weightology to a point where I could start putting a little money into trading again I jumped back in. I’ve been doing really well ever since. Recently Chad heard how well I was doing trading, we started talking, and we both realized that there was a big need in the fitness industry for financial education from everything to debt management, investing, and even doing some trading.

Matt: Thanks for the overview guys. I was really interested in reaching out to you both because I think our missions have a strong overlap. The mission behind StrengthPortal is to help personal trainers have long-term careers in this industry and blow the average career length of less than three years out of the water. I’d love to hear more details about this new venture you’re starting, Fit Pro Financial. What stage is the venture at? What will the business look like in 6-12 months?

James: We’re currently in the building phase. We’ve pushed a landing page live. You can go to Fit Pro Financial and sign up for the email list. I’m currently building the website behind the scenes and hope to have it live in a month or two. To get specific, Chad and I are working on building out an educational course for fitness professionals that will assist them with their financial management. We’ll have sections in the course about debt, how to take out loans, when you shouldn’t take out a loan, etc. We’ll be touching on concepts like emergency funds, retirement planning, 401 k investing, general investing, and so on. We’re going to cover a lot, so yeah we’re still in the building phase. We’re even planning on having a webinar soon to go more in depth on our plans.

Chad: Yeah, the webinar is a new project for us. We were originally going to announce our plans with Fit Pro Financial at the Inland Empire Fitness Conference in Spokane. James and I have both spoken at the event for the last few years and I was actually the MC of the whole thing last year. This year we were planning on giving a whole presentation, but the event was cancelled due to Covid-19. So, we are going to repurpose the educational content with this webinar. I’m really looking forward to doing this so we can get these concepts out to our friends in the industry. There’s just so much content to create courses on. I think eventually we will morph into more of a community where you can talk about the content we’re putting together and work on putting all this new knowledge into action.

Matt: Awesome, well definitely let me know when the webinar and course launches are happening so we can share that with the StrengthPortal channels.

I’d like to get a bit more specific about the course content, if you guys don’t mind. One thing that is really unique about the fitness industry is that there is a really low barrier to getting started as a personal trainer. Essentially you can graduate from high school, get a personal trainer certification, get hired at a big box gym chain, and start working right away. Within 6-12 months you could be making $40,000 or in some cases up to $60,000-$80,000. So, to bring this back, if there was a personal trainer in their early 20s who’s never been exposed to any financial education what would your number one tip be for them?

Chad: The first thing that I would say, because I lived through it myself, is that you have to learn how to not spend money on unnecessary things. You need to avoid getting into debt. If you have to start making credit card payments or car payments on interest it’s going to take away your ability to save. The crazy thing is that if you’re young you really don’t have to save that much money to have a big impact on your finances in the long-term. If you save $5000 each year in your twenties, invest it, and get normal returns until you reach retirement age you will end up with an incredible amount of money. With this small investment early on you end up having the ability to buy houses, buy a fancy car, and have financial freedom. Unfortunately, we’ve all seen young personal trainers start spending all of their money since they are making so much at a young age. They start wanting to buy a nice car, go out all the time, and they want to flash their money a bit. When I was a young personal trainer I went into debt and I know just how much it hurt me. It’s not just trainers, just people in general. You keep on buying and buying and then you start stacking on debt on top of that. It’s really hard to get out of that cycle. So, if you learn that first lesson to save and not spend as much it will open so many opportunities for you financially down the road. You can start to invest, potentially open a business, and so on. You won’t have the opportunity to do any of the fun stuff later on if you’re stuck in debt. One thing to add to that is that we’re seeing just how important it is to have an emergency savings fund right now with Covid-19. When something crazy like this happens, gyms are closed and there’s no money coming in, you need something to fall back on. In the long-term we’re all going to experience periods like this, so having good spending habits and a safety net to fall back on is incredibly important.

James: To add to that, Chad and I have both made these exact mistakes before. It’s not like we’re highly educated financial advisors, we’ve experienced all of these mistakes and lessons as fitness professionals (laughing). I’m a perfect example of what Chad is talking about. In college I had credit card debt and a terrible credit score. I think it was in the 500s. Now, I have a credit score in the low 800s and the highest score you can get is 850. So, we’ve learned this all the hard way and we really care a lot about helping personal trainers avoid these mistakes themselves. Along with the tip from Chad on the importance of saving, I think another incredibly important lesson to learn early on is that you need to prioritize paying yourself. I made this mistake when I became a full-time day trader. I wasn’t regularly taking money out of my trading accounts to pay myself. As my investments grew and grew I got more and more cocky. When everything blew up on me I ended up with nothing. I took that lesson and when I started trading again over the last few years I set up a payroll system to pay myself regularly from my trading accounts automatically so I didn’t make the same mistake again. To drive that home, if you’re putting an emphasis on paying yourself that will make it easier to save money, invest into your retirement funds, and so on. If you make a plan to do all of this systematically it makes a big difference in the long-term. It's the exact same thing as working with a client to help them lose weight, you need to make a plan. You need to have a calorie and macro budget.

Chad: Yeah, I agree with that completely. James and I talked a lot about how we should present this information so that it has the highest possible impact for fitness pros and the analogy with macros is a good example. We expect all of our clients to follow our plans, track their calories, and their macros. When we check in with them we are confused as to why it can be so difficult for them. It’s interesting because if we looked beyond our clients health and fitness you’d see that they are implementing all of these successful habits that have helped them become wealthy and as fitness professional we’re not making or following any plans to get the same results with our money! We don’t want to put ourselves on a budget, we don’t want to be told how much we should spend when we go out, and so on. There’s no difference. With Fit Pro Financial we’re going to be making plans that will set ourselves up for long-term financial health, just as we do with our clients with their fat loss.

Matt: The two of you just shared a ton of great lessons directly from your own experiences. Using the language of fitness to educate fitness professionals makes a ton of sense to me because there are so many parallels. One lesson the two of you just emphasized that really stood out to me was the value in making these investments earlier rather than later and how your investments can compound. Personal trainers tell prospects and clients all the time that the earlier you invest in your health and fitness the more you will benefit from the work in the long-term. To add to that, personal trainers have clients in their 40s, 50s, and 60s all the time who are just getting started and it’s important to know that it’s not too late. The most important thing is to get started and the sooner the better.

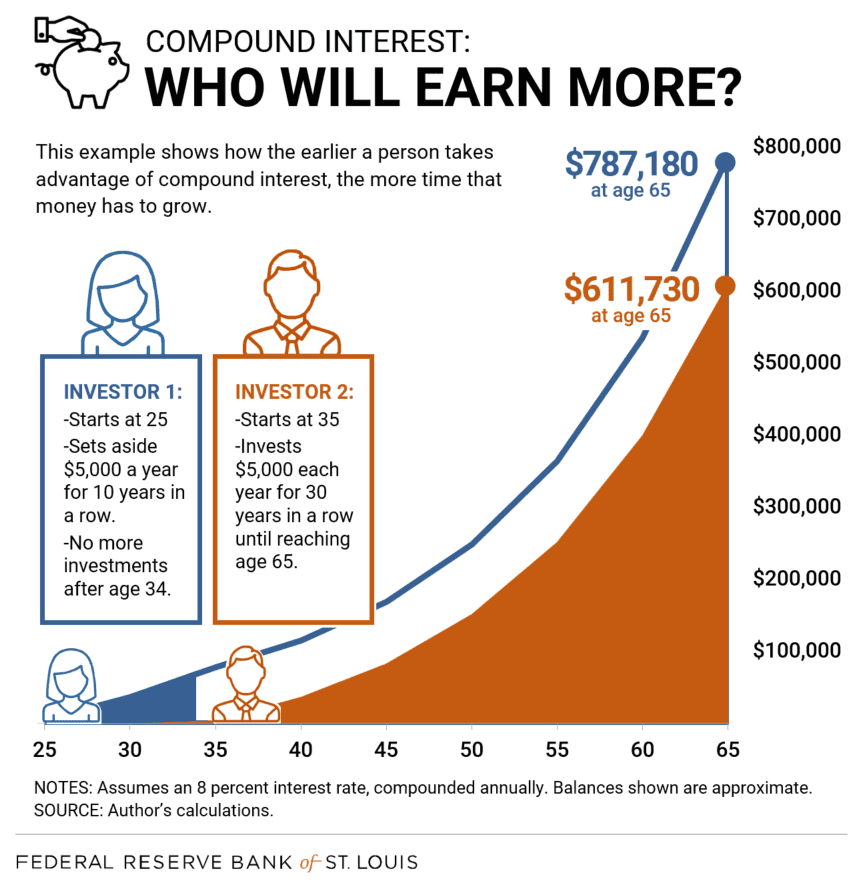

James: Absolutely. This chart that Chad found really shows how big of a difference it can make in the long-term if you start investing early:

Unless you’ve experienced the power of compounding it’s really difficult to understand. The early you start the more you’ll benefit from the investment. The hard part is having that long-term thinking.

Chad: For people who may not know, what we’re talking about here is investments compounding so you can make interest on your interest. A quick example, if you have $1000 to start with and it grows 10% over a year you now have $1100. Well, the next year if your investment grows 10% again you’re not making 10% on $1000 you’re making it on the $1100 so it becomes $1210 and so on. Over the long-term, if you have the ability to make interest on your interest you’ll end with an incredibly large amount far beyond your initial investment. When I buy stocks I make investments with a long-term mindset and look for stocks with dividends to maximize my earnings. When I get these dividends I don’t cash out, I reinvest them into more shares in the company so the size of my investments and their value grow and grow. We want fitness professionals to experience the positive benefits of compounding interest, instead of only experiencing the negatives from stuff like credit card debt. If you’re only paying the minimum for your credit card debt there’s a reason you never get out of debt. So, just like you were saying, it’s never too late to get started, but there are huge benefits to starting as early as you can because of compounding growth.

James: Another example to think about here is the growth of the Covid-19 virus itself. I think most people understand that if one person is infected, they can infect two people, and that grows exponentially from there. That’s how compound growth works with your money, it’s the same concept. It’s not additive, the growth multiplies.

Matt: Absolutely. To continue off the question earlier, let’s say you’re talking to a personal trainer who is looking to move beyond working as a personal trainer employee for a big box gym and wants to start a business for themselves. Both of you run businesses of your own, so I’d love to hear your advice for someone looking at taking this next step.

Chad: I would advise taking an approach similar to what James did with his paper trading. For a year he practiced trading day after day to learn and to prove to himself that he was ready to start trading with actual investments again. There’s a lot you can, and should do, before you open your own facility. The first thing you can do is that while you’re an employee of a gym you can start saving money. You’re going to learn that there’s a lot of required costs upfront to getting something started. Second, you can go through the entire process of starting a business on paper. Write a business plan, go out and find out what the costs and expenses for fitness business owners are, and ask questions. You’re going to learn so much from going through this process. The biggest mistake I see a lot of fitness professionals make when they go out into business on their own is that they don’t realize until after they’ve started just how much work it is. They make the move before learning about all the different aspects of what it takes to run a successful business and find out that they really don’t enjoy doing things like marketing, running payroll, and so on. They may be an excellent trainer, but are they good at things like finding and motivating employees or local advertising? You need to map out everything to see if this is an unrealistic idea or a viable business that will provide a strong financial return for you. By going through this process you may find that you make more money as an employee for someone else than you do as a business owner! There’s nothing wrong with that. Having said that, if you go through the steps of making a plan, saving money, and have reduced your risk you should feel confident getting started.

James: Absolutely. The only thing I’ll add to that when you start a business everything is going to take a lot longer than you think (laughing). You’re not going to be up and running in a few months. Whatever timeline you have, double or triple it. You have to have projections and be prepared for all possible scenarios.

Chad: Yeah, it’s definitely going to take twice as long and cost twice as much. I really feel bad for anyone that has opened a facility in the last 6-12 months because they’ve got to be hurting. I know how bad I’m hurting and I’ve been open for 17 years. If you have a new business, have debt, and haven’t had a chance to build up your clientele you’re in a really tough spot right now.

Matt: Yeah, 100%. The fitness industry has been completely disrupted with this crisis and we all have friends in the industry that are really hurting right now.

I do think that’s a really important point though, that you can get your reps in and learn before making the jump to owning your own business. It’s absolutely possible to do that. At the same time, from a financial standpoint all of the habits you should have as a personal trainer are the same. You have to make a plan, be consistent, and when you are making consistent revenue or income protect the downside for situations like this and save. You don’t want to be overexposed.

Let’s go back to the happy path. So let’s say that as a personal trainer or fitness business owner you’ve built up the right saving habits and are hitting your revenue and income goals. What comes next from a financial standpoint? What type of advice would the two of you be passing along to someone who has money to play with right now?

Chad: James and I are both in this position right now because we’ve worked hard for years and have cash available. If you’re in a similar position in your career then what you should know is that since the 1920s there are very few investments that have consistently earned you more than putting your money into the stock market. It’s impossible to say when the bottom is going to hit the market as a whole during the Covid-19 crisis, but there are a lot of stock prices that may never be this low again. It’s a really interesting time in the stock market with a ton of volatility. I’m seeing my retirement accounts going up and down by a thousand, sometimes tens of thousands, every single day. Despite this all, I’ve still been purchasing stocks I like continually over the last few weeks because I’m a long-term investor and don’t worry about day to day fluctuations. It all depends on the level of risk you want to take on, but there are strategies for every type of investor right now. Whether its index funds or individual companies, we’re investing with the money that we had saved up for an opportunity like this. My only regret with all of this is that I wish I had this advice back in my twenties and had started sooner so I’d have even more money right now to take advantage of the stock market.

Matt: James I want to piggyback off of that and throw the same question to you. It seems like you and Chad both are advising that if you have money saved this is an incredible opportunity to invest, but you have different approaches.

James: Yeah, so I wouldn’t recommend my approach for the vast majority of people to be honest (laughing). Day trading and swing trading is probably the hardest thing you could ever do. One quote that’s really stuck with me is that “trading is the hardest easiest way to make money.” It’s really easy to push buttons, which is all you’re doing when you boil it down. You’re just pressing buttons to buy and sell and seeing your money change, but it’s obviously difficult because only a small amount of people can do it well. It’s kind of like long-term weight loss statistics, only around 5% of people are able to maintain a 10% weight loss after a year. Most day traders try doing this for a few months and give up. For me, I’m taking advantage of volatility in the market right now. I will say that if you want to compound your money, nothing compounds it like day trading. In 2020 alone I’m already up 150% so far. At the same time, it’s very risky and I have to mitigate this with a really solid plan to back it up. Every trade I take has a stop loss and I will not deviate from my plan no matter what. It’s taken me years to get to this point, so I usually recommend against this approach. Having said all that, it’s important to know that with all of my day trading profits I’m going to be taking a certain amount to reinvest into long-term stock purchases just like Chad. I’m following the plan and putting money into my retirement accounts, just like we will advise people to do through Fit Pro Financial. Those accounts for me are mostly diversified Vanguard funds that are actively managed, stocks, and corporate bonds. So, my short-term trading is radically different from what Chad is doing, but my long-term stuff is very similar.

Matt: So just to frame that a bit further for fit pros, it sounds like what you’re doing with the day trading is the high-risk and high-reward final level of trading if you’ve earned that opportunity from a financial perspective.

James: Exactly. It’s like you’re playing Quake and you’ve reached the final boss (laughing).

Matt: So the entry point for most fitness pros is probably these retirement investment accounts and a long-term approach which both of you are advocating for.

Chad: Yeah, absolutely. Like he said, James’s returns are unbelievable, but he has to treat it like his job. He has to pay attention to that everyday and has very specific rules he follows. It’s a lot of work. For most personal trainers and business owners they won’t have the time for that. What they should be doing is first saving up an emergency fund and putting it into a savings account for situations just like Covid-19. Don’t ever take that and put it into investments, because it is possible to lose money short-term and long-term in the stock market. A good example of that recently was a company called Luckin Coffee. Everyone was advising that it was a good buy, but the stock recently tanked and almost went to zero because it turns out the company was cooking their books and lying about their incredible profits. So, never touch your emergency fund and make sure you are protected, but once you have money beyond that you can take on the risk, and potential rewards, of investing long-term. Get started with retirement accounts, max those out, and then you can move on to investing with you play money. You should be in a position where if your play money went to zero, you won’t feel the pain. Even though the market is going up and down right now you should be sleeping well. Index funds are a good place to start there, but the sky really is the limit for where you want to take this. James’s day trading is like being a pro bodybuilder where you really have to put your all into it. My approach is like fitness for a general population client. This is a long-term process we’re committing to so I’m going to be fit financially for the rest of my life.

Matt: That’s a great way to frame that for personal trainers and probably a good note to end on (laughing). I really appreciate both of you sharing your time for this interview and am really excited to see what you do with Fit Pro Financial. I know just how important it is, so keep up the great work!

If you’d like to follow Fit Pro Financial please check out the links below:

Subscribe to StrengthPortal Blog

Get the latest posts delivered right to your inbox